Payment Fraud Solution

Payment fraud is one of the top threats facing organizations today.

It costs businesses an average of $125,000 per incident, and nearly one in three finance leaders now rank it as a critical enterprise risk (Ardent Partners).

Corcentric’s StopFraud™ solution unites advanced technology with hands-on expertise to protect every stage of the AP process—from supplier onboarding to payment execution. This service-driven approach ensures every transaction is validated, every payment secure, and every team supported.

The Corcentric Difference

Corcentric’s StopFraud™ solution goes beyond software to deliver service-driven payment protection. It’s a hands-on approach that blends multi-factor validation, continuous supplier enrollment, and expert oversight—so your team never faces payment risk alone. Built on industry-standard banking safeguards, the StopFraud™ Validation Framework adds continuous monitoring, AML screening, and audit-ready controls for complete confidence in every transaction.

Our Four Pillars

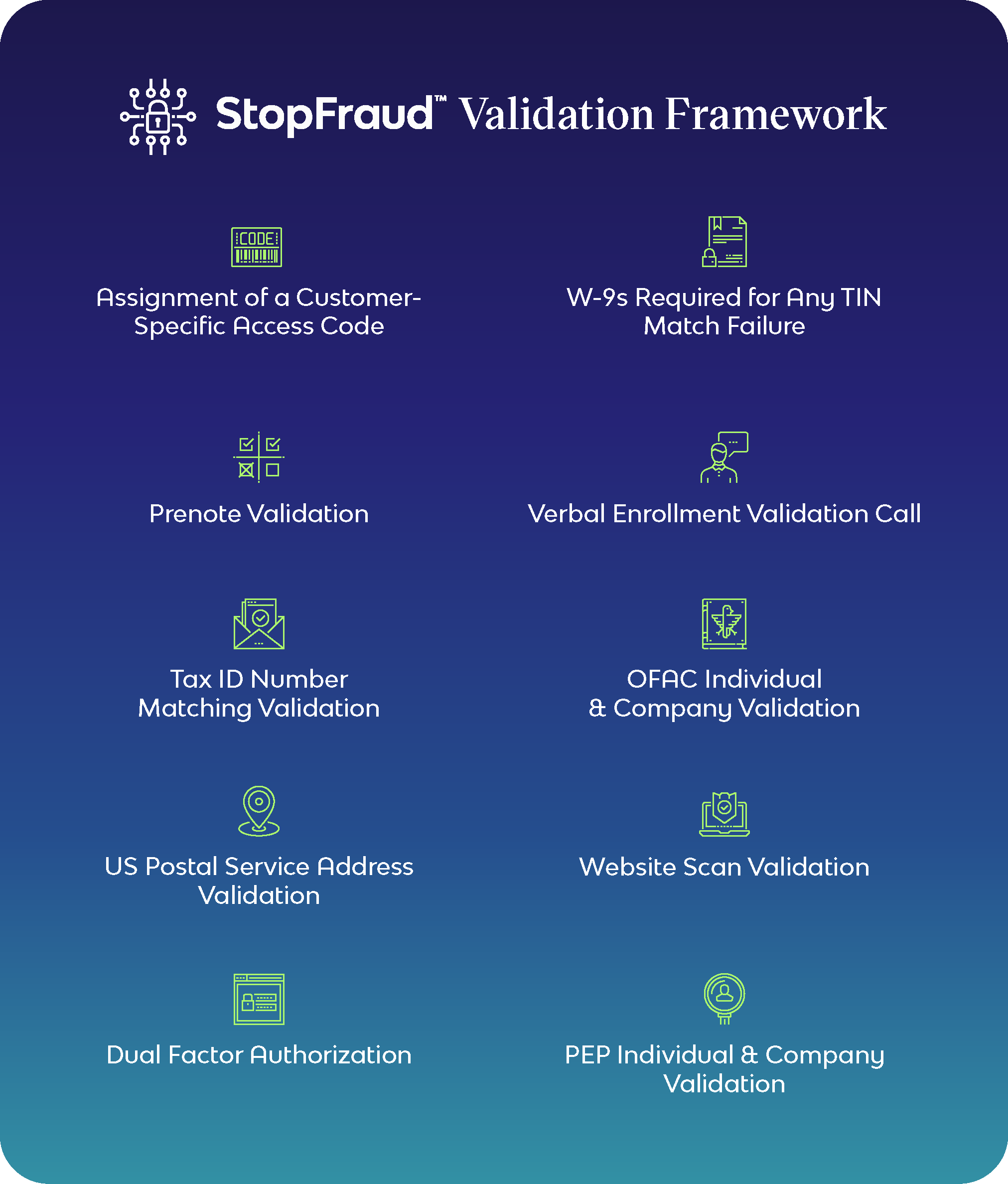

StopFraud™ Validation Framework

A multi-factor, layered defense that combines advanced validation technology with human expertise to deliver the ultimate protection against payment fraud.

Exceptional Service + Care

Dedicated experts support clients and suppliers with onboarding, monitoring, and resolution — ensuring lasting protection at every step.

Fraud Stops at Onboarding

Suppliers are validated upfront and continuously re-validated to ensure only trusted partners stay in your network.

Spend Optimization

Corcentric helps organizations achieve the right balance of payment methods—maximizing rebates, minimizing costs, and reducing fraud exposure.

StopFraud™ combines advanced validation technology with hands-on service to deliver unmatched protection against payment fraud. This multi-layer framework unites automation, analytics, and expert oversight—blocking fraud before it ever reaches your AP process.

Unlike providers who rely on limited checks or after-the-fact detection, Corcentric pairs intelligent automation with real people who verify supplier enrollment, credentials, and payment details. This layered defense ensures:

Stronger security – Fraud is intercepted at the source, delivering protected ePayments and reducing risk exposure.

Reduced fraud costs – Every safeguard prevents revenue loss before it happens.

Less AP workload – Automation handles the routine; experts resolve the exceptions.

Greater confidence – Every payment passes through Corcentric’s proven validation framework—supported by a team that stands behind every transaction.

Result: Smarter automation. Human assurance. Complete payment protection.

Industry-Grade Compliance & Controls

Corcentric’s StopFraud™ Validation Framework goes beyond fraud prevention—it’s built for financial integrity. Every layer combines banking-grade protocols like continuous transaction monitoring, AML and sanctions screening, and audit-ready documentation. This unified approach safeguards payments, satisfies internal compliance standards, and helps organizations stay prepared for external audits and evolving regulatory requirements.

Proven Impact

$5.7M+

in fraud prevented with StopFraud™

Invoice costs reduced by

80%

Cycle times cut by

82%

Exception rates lowered by

59%

Customer Voice

“Technology is critical, but people make the difference. Corcentric’s team caught a fraudulent supplier email that automation alone would have missed.”

AP Manager, National Restaurant Chain

FAQs

When unauthorized or deceptive transactions slip through the cracks, they drain financial resources. Payment fraud can take many forms, from credit card fraud and wire fraud to more insidious tactics like phishing schemes and fake invoices. Each method is designed to exploit vulnerabilities. The consequences? Potentially devastating. Beyond the immediate hit to the bottom line, payment fraud can erode trust, damage reputations, and burden companies with costly recovery efforts. As digital commerce grows, so do the threats, turning payment fraud into a persistent and evolving risk for businesses everywhere.

Common types of payment fraud that target companies include:

- Phishing attacks: the art of digital deception Phishing attacks are a masterclass in manipulation, using deceptive emails or messages to lure unsuspecting employees into sharing sensitive financial information. These messages often masquerade as legitimate communications from trusted sources—vendors, partners, or even internal departments. A single click on a malicious link or attachment can expose company bank accounts, credit card numbers, or login credentials. Once fraudsters gain access, they exploit these details for fraudulent transactions or further attacks. Phishing remains a leading threat because it preys on human error, proving that even the most advanced cybersecurity measures are only as strong as an employee’s vigilance.

- Business Email Compromise (BEC): when fraud takes a personal approach With BEC attacks fraudsters slip into the digital identity of a company executive or trusted supplier. They send out emails that appear genuine, urgently requesting payments or wire transfers. The deception works because it feels personal, often exploiting real relationships within a company. A CFO might receive what seems like an authentic email from the CEO authorizing a critical payment. By the time the fraud is detected, the money has often vanished into untraceable accounts. BEC attacks are particularly insidious because they bypass standard phishing red flags, making them difficult to spot until it’s too late.

- Invoice fraud: when the bill isn’t real, but the losses are Invoice fraud is a numbers game—and fraudsters play it well. They submit fake invoices, hoping that busy accounts payable teams will process payments without a second thought. Sometimes, they create entirely fictitious companies; other times, they impersonate legitimate vendors with subtle tweaks to payment details. The result? Companies end up paying for goods or services that were never delivered. In some cases, fraudsters even intercept real invoices and alter payment information, diverting funds to their accounts. For businesses, detecting this type of fraud can be a logistical nightmare, with financial losses stacking up before anyone realizes they’ve been scammed.

- Credit card fraud: swiping more than just your money Credit card fraud is a fast and ruthless operation. Armed with stolen card details—whether hacked from an online database or skimmed from a point-of-sale system—fraudsters make unauthorized purchases, often within minutes of obtaining the information. For businesses, these fraudulent transactions can pile up quickly, especially in e-commerce environments where card-not-present transactions are common. Beyond the immediate financial impact, companies face the headache of chargebacks, which come with fees and lost revenue. Even more concerning is the potential damage to customer trust. When credit card fraud hits, the ripple effect can hurt a company’s reputation as much as its bottom line.

- ACH/wire transfer fraud: a high-stakes game with no reset button ACH and wire transfer frauds are the heavyweights of payment fraud, often resulting in large-scale financial losses. Fraudsters use tactics like social engineering or account takeovers to initiate unauthorized transfers. Once the money is sent, it’s almost impossible to retrieve—it vanishes into accounts designed to be untraceable. Because wire transfers and ACH payments are often irreversible, businesses are left holding the bag. The speed and finality of these transactions make them prime targets for fraud, leaving companies scrambling to tighten security and verify payment requests before it’s too late. This type of fraud is particularly damaging because it often flies under the radar until the money is gone.

Payment fraud doesn’t just hit the balance sheet—it ripples through every corner of a business. The immediate impact is often direct financial loss, but that’s just the beginning. A company’s reputation can take a significant blow, eroding trust among customers, investors, and partners. In industries where compliance is critical, fraud can trigger regulatory penalties, adding another layer of financial strain. Beyond the dollars and cents, payment fraud can derail daily operations, forcing teams to focus on damage control instead of growth. Legal battles may follow, with costly lawsuits or settlements dragging out the ordeal. Ultimately, payment fraud can leave long-lasting scars that go far beyond the initial financial hit.

Detecting fraud requires businesses to stay one step ahead by keeping a close eye on unusual patterns. Sudden shifts in transaction behavior—like unexpected spikes in spending or irregular payment amounts—can be early red flags. Requests for payments to unfamiliar accounts should immediately raise suspicions, especially when the account details have never been used before. Invoices with inconsistent or unusual details, such as discrepancies in amounts or vague descriptions of services, are another signal that something might be off. Fraudsters often slip up by using email addresses or contact information that doesn’t quite match the known suppliers – a telltale sign that the person on the other end may not be who they claim to be. By monitoring these indicators, businesses can catch fraud before it causes serious damage.

Payment fraud isn’t just an inconvenience—it’s a ticking time bomb. To defuse it, consider these key strategies:

- Start by locking down your financial accounts with multi-factor authentication (MFA). It’s like adding an extra deadbolt to your digital vault. Next, double-check any large payment requests through a secondary communication channel—phone, video call, anything but email. Fraudsters love exploiting weak links, and human error is often the biggest.

- Your employees are your first line of defense, so train them like it. Equip them to spot phishing attacks and shady requests before they become financial disasters. And don’t forget encryption. Any sensitive financial data should be encrypted—no excuses.

- Set clear transaction limits and approval workflows to make sure large sums aren’t flying out without oversight. Finally, keep your system in fighting shape. Regular audits of your payment processes will help you catch vulnerabilities before they’re exploited.

- In the battle against fraud, proactivity beats recovery every time.

StopFraud™ verification program ensures:

The StopFraud™ verification program is your frontline defense against payment fraud, designed to ensure every transaction is secure and legitimate. It guarantees that payments go only to the correct, verified vendors, eliminating the risk of falling for imposters. With StopFraud™, each payment is carefully checked to ensure it matches the exact, approved amount, so no funds slip through unnoticed. It also eliminates the risks associated with handling and storing sensitive supplier bank information, keeping that data secure and out of reach for fraudsters. Continuous monitoring ensures that every payment is successfully delivered, providing peace of mind and reinforces your financial security.